|

LEAFLET 1

BRADFORD & BINGLEY BUILDING SOCIETY

FRAUD & CONSPIRACY

B & B USED A FRAUDULENT RECORD OF ACCOUNT IN ORDER TO TAKE POSSESSION OF A WIDOWS HOME.

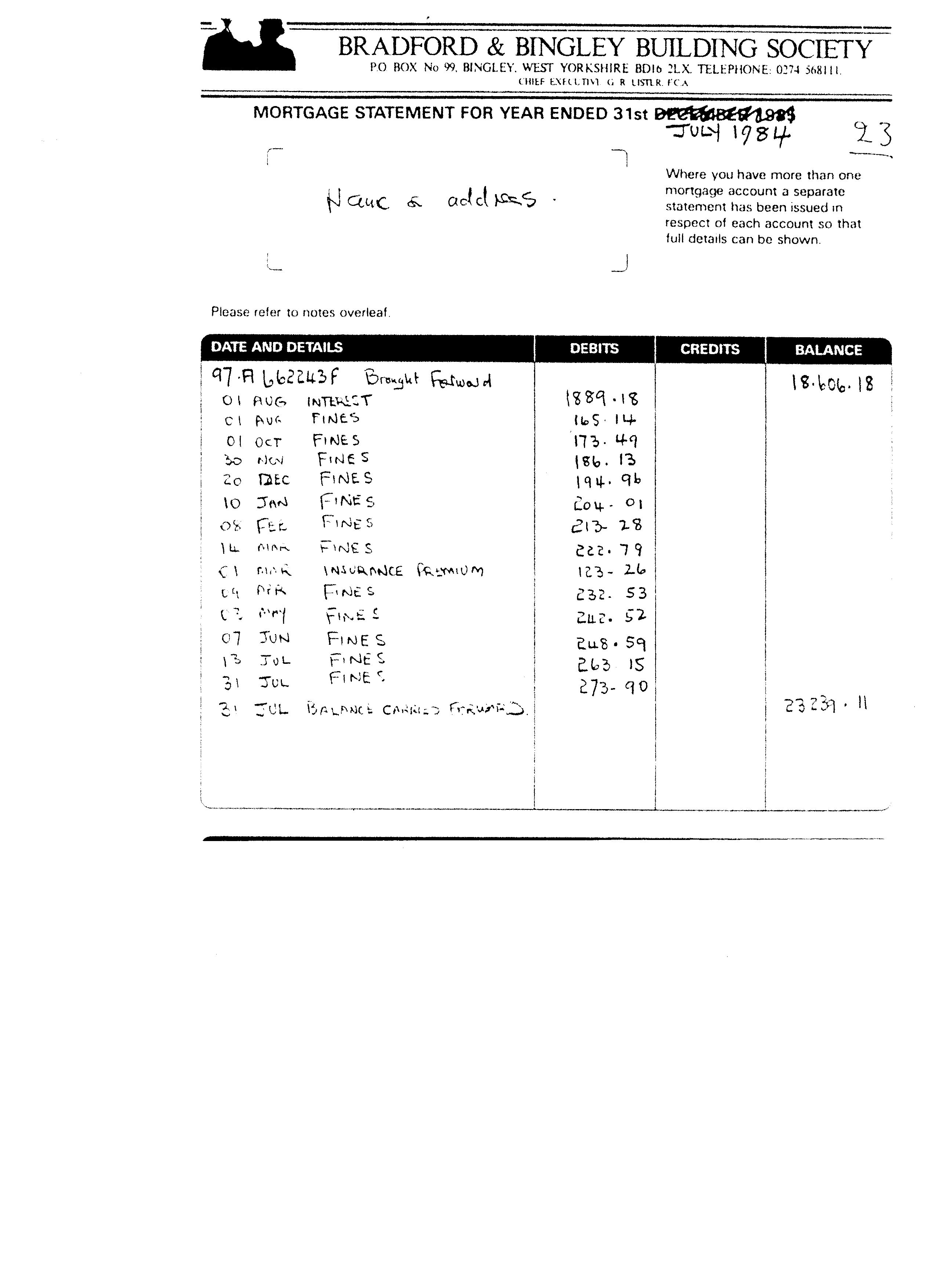

Below is one of the source mortgage statements that were produced by Bradford & Bingley (B&B) in late March 1986 but not disclosed until 2000, nearly three years after the repossession in 1998. On its own it is uninformative and lacks the information needed to test its authenticity. In order to test these alleged figures the following information is required.

The interest rate that was applicable at the start of the financial period, and a record of any interest rate changes that had taken place within the alleged financial period.

A repayment schedule calculated to meet the completion of the mortgage within its lifetime.

The amount of arrears at the start of the period and a closing balance of arrears, all mortgages have an arrears account that runs parallel to it in order to track early as well as late repayments.

The above information can be had from other spurious documents supplied by B&B over the years and are as follows.

The interest rate at the start of the period was 14.5% followed by a rate reduction of 1% as of 1st March 1984. These rates mean that the figure entered at 1st Aug 1983 if authentic would be Ż2,697.89. This figure would have to be reduced by Ż46.51 to represent the reduction of 1% for the final three months of the period, producing a total of interest for the period of Ż2,651.38. Making the interest figure of Ż1,889.18 applied by (B&B) clearly false M.I.R.A.S. was not applicable to this account.

Using the interest figure of Ż1,889.18 that (B&B) have suggested. Any repayment schedule would have to take into account the interest added, an insurance premium of Ż123.26 added on 01st Mar, and a further amount for the reduction of the alleged debt. Given that this account is supposed to be in its fourth period of a 20 Year term for what was originally a Ż12,000.00 advance this would have to be a substantial reduction. The interest and insurance premium total Ż2,012.44. The repayment the fabricator has decided on is Ż2,004 for the period, thereby increasing the debt. Clearly a computer could not have generated the alleged repayment figure.

The arrears balance at the start of the period is claimed to have been Ż6,605.59 with a closing

balance of Ż11,230.08 as at 31st July 1984. The closing balance on the account is recorded as Ż23,239.11.

This suggests that if at the 31st July1984 the alleged arrears were to be paid in full the balance on the account would be Ż12,009.03. It is not possible that an account could be greater after four years if it had been brought up to date.

Fines to the bank are a means of colleting any interest lost as a result of any missed payments within a financial period. Each fine is calculated to bring any such losses up to date at the time the fine is applied along with any administration fee that may be applicable.

It follows that a fine could not be applied on the first day of a financial period because interest has only just been calculated for the whole outstanding balance on that date, and no payments could have yet been missed within the period.

Fines are also variable in amount which is determined not only by the amount of arrears but also the amount of time since the last default. On this statement the entry of Ż273.90 on July 31st only covers a period of 18 days when it could never be calculated to be greater than the one entered on July 13th for a period of 36 days since the last default.

This is simply not a record of anybodyÆs mortgage account. It is a fabrication that was used to fool the courts into thinking there was an ongoing record of account that did not exist. The original conspiracy to produce this document involved only a small number of people. Many more are now fully aware of this deception but refuse to deal with it or discus it with any level of honesty.

LEAFLET 2

Why Bradford and Bingley Building Society Found it Necessary to Perpetrate This Fraud

Bradford & Bingley (B&B) took over the affairs of Merseyside Building Society (MBS) on 31st March 1985. Mr Landsbury Laurie was the Secretary and only full time employee of the MBS. He was responsible for dealing with all mortgage accounts.

B&BÆs first contact with Mrs. D was in Dec 1985, 9 months after the transfer.

Mrs D has always claimed that no account should have been transferred following a dispute with MBS. There had been no contact with MBS for the 4 yrs and 7 months prior to the transfer on Mar 31st 1985, no demands for payment of capital or arrears and no court actions during this period. If this account had been in place as suggested by B&B, repossession would have taken place prior to the transfer.

B&B had decided that a debt of Ż25,149.93 should have been transferred to them and that by Dec 31st1985 this amount had increased to Ż27,166.27.

Mrs DÆs solicitor (Silverbeck & Co) sent a letter dated 21st Mar 1986 to B&B requesting how the figure of Ż27,166.27 had been arrived at from an original advance of Ż12,000 on 1st Aug 1980.

For B&B to explain how these figures had been arrived at, and to pursue a claim for repossession a record of account would be required, this would normally have been a straight forward request for the accounts dept had the account existed.

The accounts dept being unable to deal with this simple request referred to internal audit for advice on what to do. A response to the accounts department dated 25th Mar 1986 was by a Mr. W.R. Wilkes in which he states;ōInt audit not interested. Simply supply Silverbeck & Co with statements as to how the figure of Ż27,166.27 is arrived at. You reply but keep me informedö.

A fraudulent set of hand written figures was now produced, however Mr. WilkesÆs instructions were not followed out to the letter and the accounts dept did not dispatch the statements to Silverbeck & Co as instructed, and instead they were sent to internal audit for approval by Mr. Wilkes.

Mr. Wilkes responded personally to the request on 1st April 1986 with a typed version of the original hand written draft. The handwritten statements were not disclosed until 2000, long after the repossession had taken place.

Although the court cases continued for the next eight years. The hearings were only sporadic, the Orders made only for the most part requesting further and better particulars from the B&B; the lack of an MBS complete record of account therefore did not become an issue. But as proceedings progressed into 1995 a letter from Mrs. DÆs then solicitor, Thelwell Fagan, dated 21st Dec 1985 touched on this very subject, saying ōwe note at this stage the absence of any accounts records from the Merseyside Building Society, and limited communications by that body to the Defendants and their then Solicitorsö.

There was no suspicion at that time or in the few years that followed that B&B was involved in the fraud that is now so obvious.

The response to the lack of MBS statements was through B&BÆs solicitor dated 26th Feb 1996 making a clear and unequivocal statement saying ōOur client holds no further information nor is it able to obtain any further documents or information. All documents relating to Merseyside Building Society were inadvertently destroyed and there is no further documentation that can be provided. They were destroyed in April or May 1985.

In a letter dated 9th April 1996 Mrs. DÆs solicitor requests evidence as to how the documents came to be destroyed and asks whether it was B&BÆs intention to call as a witness at the trial of action Mr Landsbury Laurie, previously of MBS and then of B&B. In their response dated 19th April 1996 B&BÆs solicitor states ōWith reference to Mr. Landsbury Laurie, he does not have any particular recollection of this matter and in the circumstances there would appear to be little point in calling him as a witness to give evidence at the trialö. This statement means that B&B alone had decided that the lack of documents somehow meant that they must have been destroyed.

B&BÆs response dated 19th April 1996 changed the whole direction of the case stating that the whole basis of the claim was that a mortgage deed was signed in 1980 acknowledging the receipt of the full amount. This statement was equally valid in 1987 yet B&B allowed the argument to continue as long as the fraudulent account was not part of that debate, a new strategy was now required.

Having only touched on what has now become clear was the most important issue in the whole case i.e. the lack of MBS records of account, Mrs DÆs solicitor made the odd decision of requesting a barristers opinion based on the evidence to date. This came back negative thereby depriving Mrs. D of legal aid. The absence of authentic MBS statements was not considered by the Barrister. B&B now amended their pleadings to strike out the Defence as frivolous. This was successful and the fraudulent account remained unchallenged.

Although appeals were made to the courts by Mrs D, B&B always applied to strike out her Defence as frivolous (to strike out became the order of the day for B&B), leaving the evidence of fraud untested. They had achieved their goal and evicted a widow from her home and left her financially ruined. Anything she tried to do was to prove costly and ineffective.

By the time the eviction took place B&B had consumed in excess of Ż100,000 of Mrs DÆs equity in legal costs.

With B&BÆs conspiracy of silence growing with time, raising public awareness to this matter of great public interest (in my opinion) is her only chance of gaining any justice in this sordid affair.

LEAFLET 3

(august 2010)

Conspiracy to Prevent Justice at Top Level in Bradford & Bingley Building Society

Part 3

In the case of Mrs. A. DicksonÆs plight for justice and her accusation of fraud and conspiracy within the Bradford & Bingley Building Society (B&B) it is apparent that knowledge of this fraud is at the highest level.

Following a letter in December 2006 to which B&B did not respond it was decided to inform the Chief Executive of B&B (Mr. Steven Crawshaw) of our intention to apply to the courts in a bid to get an explanation as to how the figures had been calculated. This letter was responded to by Karen Slinger of the Office of the group Chief Executive stating that she had been asked to respond by Mr Crawshaw on his behalf and she states, ōBradford & Bingley will refute any allegation made and will apply to strike out any claim Mrs. Dickson pursuesö

Clearly Karen Slinger would of tested the evidence and answered it if it had been possible for her to do so, after all it is a simple question as to how the interest on an account has been calculated, which is something that should be able to be done by any account holder at branch level, without a treat of further legal costs to the account holder.

There is no shortage of names of people within (B&B) who have been questioned about this account and are fully aware of this fraud and chosen to remain silent, lied when responding to the questions posed, or simply avoiding answering the question posed, the following names included;

Mr. D. Robson, Mr. C. R. Hughill, Mr. Mark Simmons, Miss. Tina Harrisson, Michael Petrie (Customer reltions officer) Chariman Mr. McKinnley.

All of these and other between them can not explain how this one account has been calculated and (B&B) only defence is to spend any equity Mrs. Dickson may have left in here property, to get the courts to strike out her claim for justice.

What sort of human beings are these?

If you would like to make any comments or require further information, please contact us at:

www.unlawfulrepossession.co.uk |